The coronavirus pandemic infused unprecedented levels of uncertainty into our economy. When the virus became more widely spread in March, businesses closed, workers self-isolated, and customers abstained from the marketplace. Even today, operations are not back to normal, and many businesses are still struggling. These changes are going to affect each organization differently, but one thing is certain: businesses hit with adverse effects from COVID-19 will need to identify the consequences on their asset base and reflect those outcomes in their financial statements.

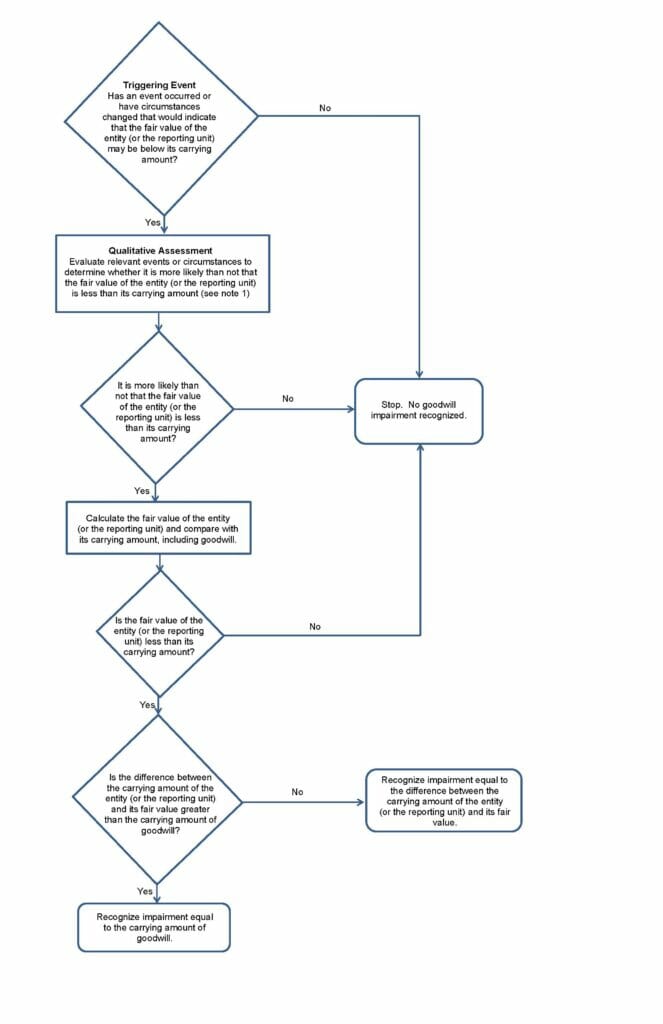

Triggering Events

External events and pressures can put an organization’s financial performance at risk. The energy sector is no stranger to this phenomenon. Just like geopolitics and changes in demand can upset the entire supply chain, the coronavirus-induced market downturns have left producers, transporters, importers/exporters, and facilitators unable to predict when their operations will fully recover. When triggering events like these have been identified, management may be required to evaluate their long-lived assets, intangibles, and goodwill for impairment.

The criterion for a triggering event is met when it is more likely than not that your asset or reporting unit’s recoverable amount (or fair value) is less than its book (or carrying) value. Determining the existence of triggering events requires significant judgment from management, and business leaders must weigh all mitigating factors to determine if the event was significant enough to meet this criterion. Triggering events can be as simple as unfavorable changes in raw material availability and prices or as severe as a natural disaster. Some common indicators of triggering events are:

- Shifts in market forecasts

- Fluctuations in materials or labor costs

- Increases in costs of borrowing

- Changes in availability of financing

- Company is experiencing or expecting future net losses in operations

- Shifts in stock prices

- Changes in management or losses of key employees

- Changes in foreign exchange rates

- Supply chain shortages

Impairment Testing

- Market Approach

The recoverable amount is determined by considering recent sales transactions of similar assets or by using market information available to the public (like a stock exchange or sale listing). - Cost Approach

The recoverable amount is determined using the cost it would take for you to build or acquire a replacement asset. - Income Approach

The recoverable amount is determined by calculating the discounted cash flows anticipated from the asset.

Regular Assets

Indefinite-Lived Intangible Assets

Long-Lived Assets

Tangible Assets

Intangible Assets

Goodwill

Reporting Requirements

Recording impairment losses will affect both your balance sheet and your income statement. In general, impairment adjustments are recorded as an impairment charge (loss) on the income statement, offset with a reduction to the asset or with a credit to a contra-asset account. If a contra-asset account is used, the asset and contra-asset accounts should be netted on the face of the financials. Impairment charges are reflected as a separate line item, if material. Classification as operating or non-operating is determined by the character of the underlying asset.

Impairment adjustments for proved and unproved reserves have more specific reporting requirements. Impairment adjustments to proved reserves should reduce the reserve’s carrying amount. When reserves have been tested for impairment as a group, the impairment can be allocated to each asset on a pro-rata basis using each asset’s carrying amount. Impairment adjustments to unproved reserves should be recorded as a valuation allowance (i.e. a contra-asset).

In addition to recording the actual impairment losses, you will be required to disclose information about how the impairment charge was determined. You should disclose in the footnotes to the financials information about the triggering events, how you determined it was a triggering event, and the methods you used to calculate the impairment.

Impairment testing is a particularly difficult task right now. Triggering events related to the pandemic likely occurred over a series of weeks or months. Should you take advantage of the simplified impairment tests? Or if you already determined that your assets have been impaired, should you report those losses in the first, second, or third quarter of 2020? And if the triggering event hit in the first quarter, should you report a subsequent event on your 2019 financials? Answers to these questions will look different for each organization. For help in addressing questions specific to your situation, contact one of the professionals at LaPorte CPAs & Business Advisors.